Where to Put Your Money in Africa as an Agri-Investor: An Analytical Investment Proposal for Africa’s Next Food-Growth Cycle

Ready

Africa’s agriculture story is often told through scarcity: hunger, drought, low yields and food imports. That story is incomplete. The more useful investment reading is this: Africa is one of the world’s largest under-built food markets, with rising demand, weak productivity, fragmented supply chains and a widening gap between what the continent consumes and what it produces efficiently.

Africa’s agriculture story is often told through scarcity: hunger, drought, low yields and food imports. That story is incomplete. The more useful investment reading is this: Africa is one of the world’s largest under-built food markets, with rising demand, weak productivity, fragmented supply chains and a widening gap between what the continent consumes and what it produces efficiently.

That gap is the investment case.

Africa’s population is projected to keep rising through the century, while urbanisation is changing diets and food-buying behaviour. Sub-Saharan Africa is expected to reach about 1.5 billion people by 2033, with roughly half of its population living in urban areas. Yet the region holds about 19% of the world’s agricultural land while producing only about 7% of global agricultural output value.

That imbalance should define the investor thesis. Africa does not mainly need more agriculture rhetoric. It needs capital deployed into productivity, logistics, processing, finance, water systems, cold chains, storage, food brands and regional trade.

The continent’s food demand is becoming larger, more urban and more commercial. Consumers are moving from purely staple-based diets toward rice, wheat products, poultry, dairy, edible oils, processed foods, fruits, vegetables, convenience foods and packaged products. But too much of that demand is still being met through imports or weakly integrated local supply chains.

For an agri-investor, the question is not whether Africa has agricultural potential. It does. The real question is where the potential can be converted into dependable cash flow.

The core investment thesis

Africa’s agri-investment opportunity is strongest in the middle of the value chain.

Primary farming matters, but it is often exposed to weather, land politics, smallholder fragmentation, weak infrastructure and price volatility. The stronger risk-adjusted returns are likely to come from businesses that solve structural bottlenecks around farmers and consumers: irrigation, inputs, mechanisation services, aggregation, storage, cold chain, processing, logistics, animal feed, seed systems, food retail, digital market access and trade finance.

The best investments will not simply own land. They will control systems.

Africa has enough land to attract investor attention, but land alone is not a strategy. Several large land-based investments on the continent have struggled because they underestimated local politics, water systems, pastoralist rights, infrastructure costs, community relations and operational complexity. The smarter investor should avoid the simplistic “buy land, grow crops, export” model. The better thesis is to invest in productive infrastructure that raises output, reduces loss, improves quality and captures value after harvest.

Agriculture in Africa should therefore be treated as an industrial platform. The continent needs food factories, feed mills, cold rooms, irrigation operators, seed companies, storage networks, testing laboratories, commodity exchanges, warehouse-receipt systems, digital procurement platforms, packaging plants, logistics fleets and branded food companies.

That is where money should go.

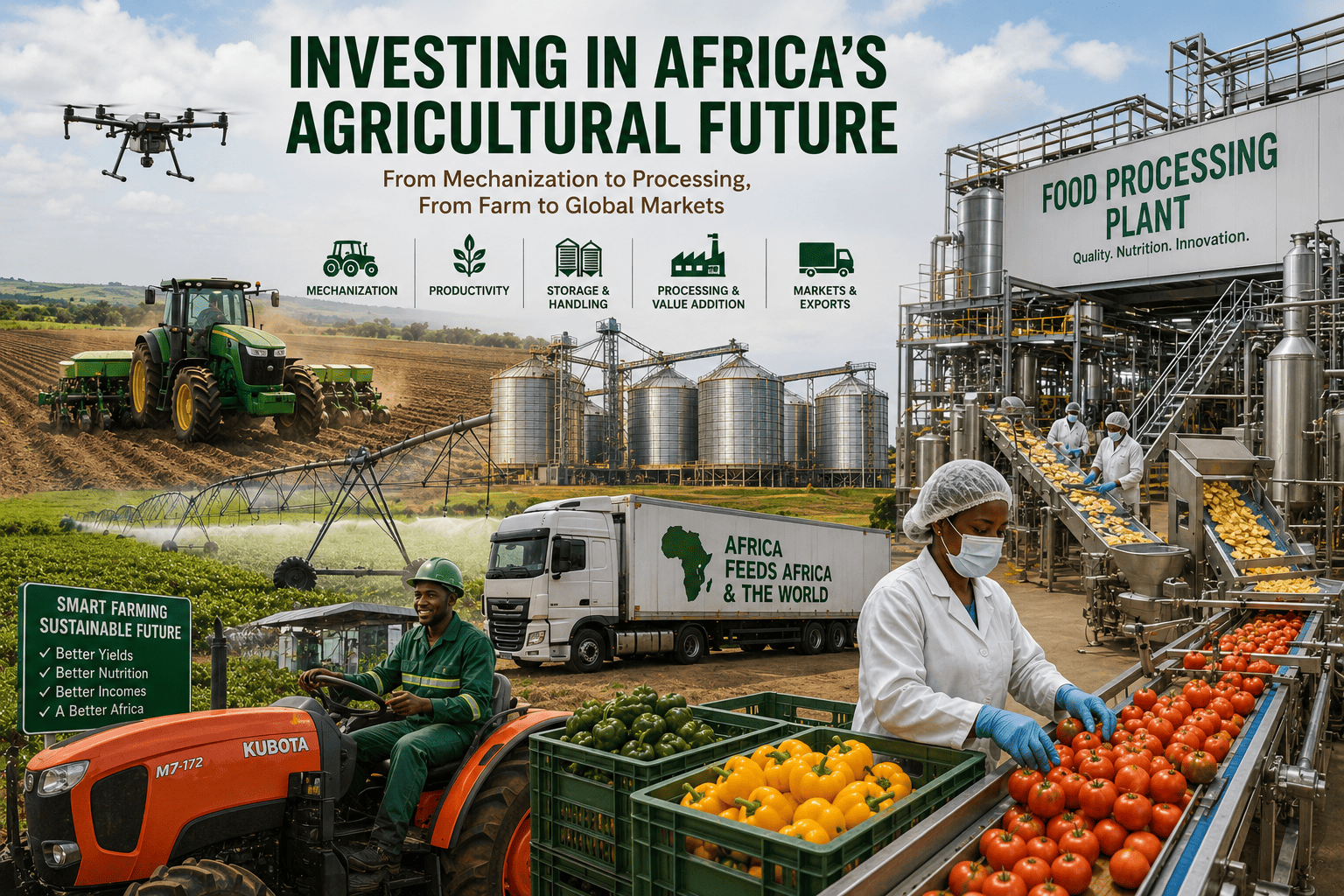

Priority investment area one: Irrigation and agricultural water systems

The first place to invest is water.

African agriculture remains heavily rain-fed, which exposes production to drought, floods and irregular seasons. Irrigation coverage in Sub-Saharan Africa remains very low compared with Asia, despite the continent’s rising food demand and climate exposure.

For investors, this creates an opening in irrigation-as-a-service, solar-powered pumps, smallholder irrigation clusters, drip irrigation, water harvesting, farm ponds, borehole management, water metering, irrigation equipment leasing and climate-smart water infrastructure.

The investable model is not only selling pumps. It is providing water reliability. Farmers pay for predictable water because predictable water improves yields, planting decisions and revenue. Governments and development finance institutions are also likely to support irrigation because water control links directly to food security, climate adaptation and rural employment.

Best markets include Tanzania, Zambia, Ethiopia, Kenya, Ghana, Senegal, Rwanda, Morocco and Egypt, depending on water availability, regulation and crop strategy.

The key risk is water governance. Investors must avoid water extraction models that create conflict with communities, pastoralists or downstream users. The best projects will combine commercial irrigation with transparent water rights, catchment management and local benefit-sharing.

Priority investment area two: Storage, warehousing and post-harvest loss reduction

The second place to invest is storage.

Africa loses too much food after harvest. Grain, fruits, vegetables, fish, dairy and meat all lose value when storage, cold chains, packaging and transport systems are weak. This is not only a food-security problem. It is an investment opportunity.

Storage creates value in three ways. It reduces physical losses. It allows farmers and traders to avoid distress selling immediately after harvest. It supports structured finance through warehouse receipts, collateral management and commodity-backed lending.

Investable opportunities include grain silos, hermetic storage, cold rooms, packhouses, aggregation centres, quality testing, warehouse-receipt systems, commodity logistics and storage-linked financing.

The best markets are major grain and horticulture producers: Tanzania, Uganda, Zambia, Kenya, Ethiopia, Ghana, Nigeria, Côte d’Ivoire and Mozambique.

The strongest model is not standalone storage. It is storage connected to buyers, processors, banks and commodity flows. A warehouse with no trade network is just a building. A warehouse connected to verified stock, credit and off-takers becomes financial infrastructure.

Priority investment area three: Agro-processing and food manufacturing

The third place to invest is processing.

Africa exports too much raw agricultural value and imports too much finished food. That is where the margin leaks. Cocoa leaves West Africa and returns as chocolate. Cashew leaves East and West Africa and returns as processed nuts. Grain leaves farms and returns as branded flour, cereals, biscuits and animal feed. Fruit is grown locally but juice is imported. Milk is produced locally but processed dairy shelves remain import-exposed in many countries.

Agro-processing is where agriculture becomes industry.

The best opportunities are in milling, edible oils, dairy processing, fruit pulping, juice production, cassava starch, animal feed, poultry processing, fish processing, packaged grains, sauces, snacks, fortified foods, baby foods, spices, coffee roasting, cocoa processing, cashew processing and ready-to-cook products.

Africa’s rising food demand and urbanisation could push the food import bill higher without investment in productivity and processing. That warning should be read as a market signal. Food import substitution is not protectionism when it is commercially competitive. It is a manufacturing opportunity.

Best markets include Nigeria, Egypt, Kenya, South Africa, Tanzania, Ghana, Côte d’Ivoire, Morocco, Ethiopia, Uganda, Rwanda and Senegal. The best countries are those with large domestic markets, stable power, reliable logistics, access to raw materials and improving retail systems.

The main risk is underestimating distribution. A food processor wins only when it secures raw materials, quality control, packaging, energy, routes to market and consumer trust.

Priority investment area four: Animal feed, poultry, dairy and protein systems

The fourth place to invest is protein.

Urbanisation and rising incomes tend to increase demand for poultry, eggs, dairy, fish and meat. Africa’s protein demand will grow, but local systems are not yet efficient enough. Feed is often expensive. Veterinary systems are uneven. Cold chains are weak. Genetics, hatcheries, dairy collection and processing remain underdeveloped in many markets.

Animal feed is one of the most strategic investment categories because it sits upstream of poultry, dairy, aquaculture and livestock productivity. If feed costs are high, protein remains expensive. If feed is reliable and affordable, poultry, eggs, fish and dairy become more scalable.

Investable opportunities include feed mills, maize-soya supply chains, oilseed crushing, fish feed, hatcheries, day-old chicks, veterinary distribution, dairy collection centres, chilling infrastructure, pasteurisation, yoghurt, cheese, powdered milk alternatives, aquaculture feed and cold-chain distribution.

Best markets include Nigeria, Kenya, Tanzania, Uganda, Ethiopia, Rwanda, Ghana, Zambia, Senegal and Egypt.

The strongest investment model is integrated but not overextended: feed plus offtake, hatchery plus farmer network, dairy collection plus processing, or aquaculture feed plus technical support. The weakest model is isolated production without control of input costs or route to market.

Priority investment area five: Horticulture, cold chain and export logistics

The fifth place to invest is fresh food.

African cities need more fruits, vegetables and fresh protein. Export markets need year-round horticulture. But horticulture is unforgiving: quality collapses quickly when cold chain, packaging and logistics fail.

The opportunity is in high-value, fast-moving crops: avocados, berries, herbs, vegetables, flowers, mangoes, pineapples, onions, tomatoes, potatoes, French beans, chillies and citrus. But the real money is often in the infrastructure around them: cold rooms, packhouses, refrigerated transport, grading, certification, irrigation, export logistics and buyer relationships.

Kenya has already shown the power of export horticulture. Morocco and Egypt have shown what irrigation, logistics and European market access can do. South Africa shows the value of standards, cold chains and export systems. East and West Africa still have room to build stronger horticulture corridors.

Best markets include Kenya, Morocco, Egypt, South Africa, Ethiopia, Tanzania, Rwanda, Ghana, Senegal and Côte d’Ivoire.

The key risk is compliance. Export horticulture requires standards, traceability, pesticide control, cold-chain discipline and buyer reliability. Investors must build around certification from day one.

Priority investment area six: Seeds, inputs and soil health

The sixth place to invest is productivity technology.

Africa cannot feed itself by expanding land alone. It must raise yields. That means better seed, better soil fertility, better agronomy, better pest control and better farmer advisory systems.

The opportunity is not only in fertilizer distribution. It is in seed companies, drought-tolerant varieties, hybrid seed, legume systems, soil testing, lime distribution, biofertilizers, precision input services, last-mile agro-dealer networks and digital agronomy.

Input systems are not a side business. They are the operating system of agricultural transformation.

Best markets include Ethiopia, Nigeria, Tanzania, Kenya, Uganda, Zambia, Ghana, Rwanda and Mozambique.

The main risk is farmer affordability. Inputs must be tied to finance, insurance and market access. Selling fertilizer or seed into a farmer's cash-flow problem produces shallow adoption. Bundled input-finance-offtake models are more resilient.

Priority investment area seven: Mechanisation-as-a-service

The seventh place to invest is mechanisation.

Most smallholders cannot afford tractors, planters, harvesters or irrigation equipment outright. But they can pay for services if those services increase productivity and arrive on time.

Mechanisation-as-a-service is better suited to African farm structures than simply selling machines. It allows equipment owners to serve many farmers, aggregate demand and generate recurring revenue.

Investable models include tractor rental platforms, harvesting services, planting services, drone spraying, land preparation, irrigation equipment leasing, small machinery for rice and horticulture, and maintenance workshops.

Best markets include Nigeria, Ghana, Kenya, Tanzania, Uganda, Zambia, Ethiopia and Senegal.

The key risk is utilisation. Equipment makes money only when it is used across enough hectares and seasons. The strongest models combine scheduling software, trained operators, maintenance, spare parts and farmer aggregation.

Priority investment area eight: Digital agriculture and market platforms

The eighth place to invest is in agricultural data and transactions.

Digital agriculture is overhyped when treated as an app-only business. But it is powerful when it solves real-world transaction problems: farmer identification, input credit, weather advisories, insurance, commodity aggregation, buyer matching, logistics scheduling, digital payments, traceability, and warehouse receipts.

New remote-sensing tools and field-mapping technologies are making it easier to understand crop area, field size, production risk and land use. Digital mapping can improve planning, finance and climate-risk management, especially in smallholder systems.

The best digital agriculture investments will not be pure software plays. They will be embedded in finance, insurance, procurement, logistics or compliance.

Best markets include Kenya, Nigeria, Ghana, Rwanda, Tanzania, Uganda, Ethiopia and South Africa.

The key risk is monetisation. Farmers may not pay directly for information. Banks, insurers, buyers, governments and processors may pay when the platform reduces risk or improves supply reliability.

Priority investment area nine: Regional food trade and commodity corridors

The ninth place to invest is in trade infrastructure.

Africa’s food problem is often regional, not national. One country has a surplus while another imports from outside the continent. One region has maize while another faces a shortage. One country exports raw produce while its neighbour imports processed goods.

The African Continental Free Trade Area can support regional food markets, but only if standards, logistics, storage, finance and border systems improve.

Investable opportunities include cross-border grain trading, commodity aggregation, bonded warehouses, inland dry ports, food corridors, quality-testing labs, digital trade documentation, regional trucking fleets and structured commodity finance.

East Africa is especially attractive because Tanzania, Kenya, Uganda, Rwanda, Burundi, Democratic Republic of Congo, South Sudan and Somalia are structurally interconnected through ports, corridors, food demand and agro-climatic diversity. West Africa has similar logic through Nigeria, Ghana, Côte d’Ivoire, Senegal, Benin and Sahelian food corridors.

The key risk is policy unpredictability. Export bans, sudden taxes and border disruptions can destroy trade margins. Investors should prioritise markets where governments are moving toward rules-based regional trade.

Priority investment area ten: Climate-smart and carbon-linked agriculture

The tenth place to invest is climate resilience.

Agriculture is both exposed to climate change and capable of generating climate solutions. Drought-resistant seed, irrigation, agroforestry, regenerative practices, soil carbon, efficient fertilizer use, water harvesting, livestock methane reduction, improved pasture management and renewable-energy-powered cold chains can attract climate finance.

That matters for private investors because climate-aligned agriculture is becoming more financeable. The opportunity is not in vague sustainability claims. It is in measurable resilience: lower water use, higher yields, reduced loss, improved soil health, verifiable carbon impact and farmer-income improvement.

Best markets include Kenya, Ethiopia, Rwanda, Tanzania, Ghana, Senegal, Morocco, Egypt, South Africa and Zambia.

The key risk is carbon-market complexity. Carbon revenue should be treated as upside, not the core business model, unless measurement, reporting, verification and buyer contracts are strong.

Country prioritisation

For a serious agri-investor, Africa should be read through corridors and value chains, not just country borders.

Tier one: strongest broad-based agri-investment markets

Kenya is attractive for horticulture, dairy, agri-fintech, cold chain, food processing, animal feed and export logistics. Its strengths are private-sector depth, finance, logistics and entrepreneurial capacity. Its risks are tax pressure, land costs, climate volatility and infrastructure bottlenecks.

Tanzania is attractive for grains, oilseeds, sugar, horticulture, livestock, irrigation, rice, cashew, pulses, agro-processing and regional trade. Its strengths are land, water potential, ports, corridors and a growing domestic market. Its risks are execution, logistics gaps, land administration and policy consistency.

Nigeria is the largest food market. It is attractive for processing, animal feed, poultry, rice, edible oils, cold chain, food brands and digital agriculture. Its strengths are population and demand. Its risks are foreign exchange, insecurity, infrastructure and policy volatility.

Ethiopia is attractive for coffee, wheat, horticulture, livestock, irrigation, agro-processing and state-backed agricultural transformation. Its strengths are scale, altitude diversity and labour. Its risks are conflict, currency and state control.

Ghana is attractive for cocoa processing, poultry feed, horticulture, rice, cassava, logistics and food brands. Its strengths are political stability and regional access. Its risks are fiscal pressure, currency and energy costs.

Côte d’Ivoire is attractive for cocoa, cashew, rubber, palm, food processing and logistics. Its strengths are export agriculture and port access. Its risks are commodity concentration and climate stress.

Morocco and Egypt are attractive for irrigation technology, high-value horticulture, agro-processing, fertilizers and export-oriented agriculture. Their strengths are logistics, state capacity and access to European and Middle Eastern markets. Their risks are water stress.

South Africa is attractive for agro-processing, wine, fruit, animal feed, food technology, retail supply chains and agricultural finance. Its strengths are sophisticated value chains and standards. Its risks are power reliability, land politics and water stress.

Tier two: high-upside but higher-risk markets

Uganda offers strong potential in dairy, coffee, grains, fish, oilseeds, animal feed and regional trade. Its opportunity is substantial, but investors must navigate logistics, land and infrastructure constraints.

Zambia is attractive for grains, livestock, irrigation and regional food supply, especially into Southern and Central Africa. Its risks are debt legacy, power and climate shocks.

Rwanda is not a land-scale agriculture play, but it is attractive for premium food, horticulture, dairy, seed systems, agri-tech, cold chain, food logistics and controlled-environment agriculture. Its strengths are execution and governance. Its limitation is scale.

Senegal is attractive for rice, horticulture, irrigation, fisheries, poultry and Sahel-facing food logistics. The risk is water, land politics and import competition.

Mozambique has large land and water potential, but infrastructure, security and fragmented smallholder systems raise execution risk.

Democratic Republic of Congo has huge food demand and land potential, especially around urban markets and mining corridors, but insecurity, infrastructure and governance risks remain serious.

Recommended capital allocation

A balanced African agri-investment portfolio should not put all capital into farming. It should allocate across the value chain.

A strong portfolio could allocate 25% to agro-processing and food manufacturing, 20% to irrigation and water systems, 15% to storage and cold chain, 15% to animal feed and protein systems, 10% to seed and input distribution, 10% to mechanisation and digital agriculture, and 5% to opportunistic land-based production where land rights, water and offtake are secure.

The portfolio should also diversify by geography: East Africa for grains, dairy, horticulture and corridor trade; West Africa for food brands, cocoa, cashew, poultry and edible oils; North Africa for high-value irrigated agriculture and export platforms; Southern Africa for grains, livestock, fruit and structured agribusiness.

The highest conviction investment theme is not land. It is infrastructure around food demand.

Investment risks

The first risk is climate. Drought, floods, heat stress and pests can destroy yields and margins. Every serious investment must include climate modelling, insurance and water planning.

The second risk is land governance. Poorly structured land deals can create community conflict, legal risk and reputational damage. Investors should prioritise transparent leases, community benefit-sharing and responsible land governance.

The third risk is policy volatility. Export bans, price controls, sudden taxes and import waivers can affect profitability. Investors should target countries with improving regulatory discipline and diversify across markets.

The fourth risk is currency. Many food businesses earn in local currency but import equipment, inputs or packaging in dollars. Currency mismatch must be managed.

The fifth risk is infrastructure. Roads, power, ports and cold chains can determine whether a good business model survives.

The sixth risk is farmer aggregation. Many business models fail because they cannot consistently source quality raw materials from fragmented smallholders.

The seventh risk is political economy. Food is politically sensitive. Governments intervene when prices rise. Investors must understand that food markets are never purely commercial.

Strategic recommendation

Africa’s best agri-investment opportunities are not in romantic farming narratives. They are in solving bottlenecks.

Invest where demand is rising but supply chains are weak. Invest where imports reveal local production gaps. Invest where climate risk is real but manageable. Invest where governments are improving infrastructure and regional trade. Invest where farmers already produce but lose value through poor storage, weak finance or lack of processing. Invest where urban food demand is expanding faster than domestic brands can respond.

The most attractive sectors are irrigation, storage, agro-processing, animal feed, dairy, poultry, cold chain, horticulture, seed systems, mechanisation services, food logistics and regional commodity trade.

The most attractive countries are those that combine demand, production potential, infrastructure, policy direction and market access: Kenya, Tanzania, Nigeria, Ethiopia, Ghana, Côte d’Ivoire, Morocco, Egypt, South Africa, Uganda, Zambia, Rwanda and Senegal.

The investor who wins in African agriculture will not be the one who only buys land. It will be the one who builds the missing machinery of the food economy.

Africa has the population. It has the demand. It has the land. It has the urgency.

The money should go where the continent’s food system breaks: water, storage, processing, logistics, finance, inputs, cold chain and trade.

That is where the next agricultural value will be created.

Uchumi360

Business Intelligence

Uchumi360

Business Intelligence

Uchumi360 covers business, investment, and economic policy across East, Central, and Southern Africa.

For the serious reader

You read to the end. That places you in a small group.

Uchumi360 is built for readers who demand precision over speed, structure over sentiment, and analysis that holds uncomfortable conclusions rather than softening them. If this work sharpens how you think about Africa's economy, help us keep building the infrastructure behind it.

Institutional Partners

Commission intelligence. Shape the conversation.

Uchumi360 works with development finance institutions, investment firms, sovereign bodies, and strategic organisations across the coverage region. Institutional partnership unlocks:

- Commissioned sector and country intelligence reports

- Branded research series under your institution's authority

- Exclusive data briefings for internal strategy teams

- Speaking and editorial presence at Uchumi360 events

- Co-published investment outlooks for your markets

Support Our Work

Independent analysis has a cost. Help us bear it.

Uchumi360 does not carry advertising. It does not take editorial direction from sponsors. Every article is produced without commercial compromise. Your contribution funds the reporting, research, and editorial infrastructure that keeps this analysis free from influence.

Secure checkout: One-time and monthly support are processed securely.

Stay Connected

Keep up with every new insight.

Follow our latest analysis, policy coverage, and market intelligence as soon as it is published. If you need something specific, reach out directly and we will point you to the right research.