Tanzania’s EV Mobility Story Is Being Built One Charging Station at a Time — But Can It Shift a Fuel-Driven Market?

Ready

The macroeconomic logic is clear. The Budget Speech says geopolitical tensions have affected Tanzania through international trade and investment, and that retail prices for petrol and diesel in Dar es Salaam rose by 44 percent and 49 percent, respectively, between March and May 2026. The government responded by monitoring fuel prices, providing diesel subsidies for May and June 2026, and committing in the medium term to accelerate alternative energy investments, including renewable energy, to reduce dependence on imported fuel.

Tanzania’s electric vehicle story is beginning to look less like a technology experiment and more like an economic policy signal.

The launch of an electric vehicle charging station in Dodoma comes at a moment when the government is trying to reduce exposure to imported fuel, deepen the productive use of domestic electricity, modernise transport infrastructure, and prepare a vehicle market still dominated by petrol and diesel engines for a cleaner and more cost-efficient future.

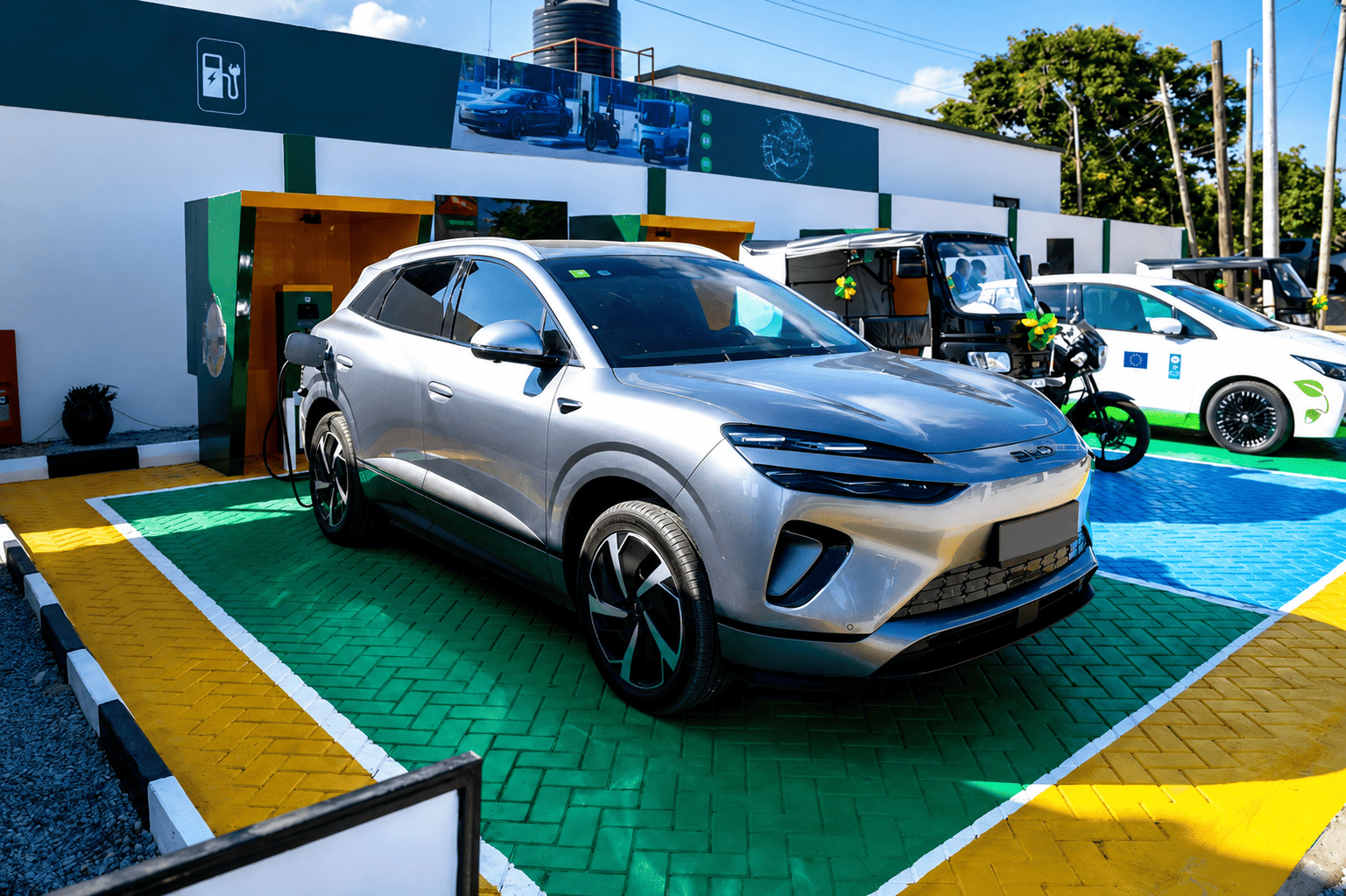

One charging station will not change Tanzania’s mobility landscape. But it can change perception. In early-stage electric vehicle markets, charging stations are not only pieces of infrastructure. They are confidence signals. They tell fleet operators, public institutions, investors, vehicle importers, banks, insurers and consumers that the market is moving from conversation to deployment.

That is why Dodoma matters.

The government’s fiscal direction is now explicit. In the 2026/27 Budget Speech, the Minister for Finance states that the government has continued to implement tax measures to promote the use of electricity in the transport sector. These include excise-duty exemptions based on engine capacity for vehicles using electricity, value added tax exemption on equipment used to convert petrol and diesel motor vehicle systems to electric systems, import-duty relief on lithium-ion electric accumulators used in assembling or manufacturing vehicles and motorcycles, and import-duty relief for assemblers and manufacturers of motor vehicles, including those using electricity, under the East African Community Assembling and Manufacturing of Goods Regulations, 2025.

For 2026/27, the most direct electric mobility measure is the proposed value added tax exemption on imported equipment used in electric vehicle charging stations under HS Code 8504.40.00. The Budget Speech estimates that this measure will reduce government revenue by 5.97 billion shillings, which means the state is deliberately giving up near-term tax revenue to lower the cost of charging infrastructure.

That is the real story. Tanzania is not only speaking about electric vehicles. It is starting to reduce the cost of the infrastructure that makes electric vehicles practical.

The budget’s broader framing matters. The 2026/27 budget is presented as the first budget under Tanzania Development Vision 2050, and it is aligned with the Fourth National Five-Year Development Plan, the East African Community Vision 2050, the African Union Agenda 2063 and the Sustainable Development Goals. The budget theme is “Building a resilient economy through digital transformation, strategic investment, and sustainable fiscal policies for inclusive economic growth.”

Electric mobility fits inside that agenda because it sits at the intersection of transport, energy, climate resilience, technology, fiscal policy and industrialisation. It is not merely about replacing petrol cars with battery-powered cars. It is about whether Tanzania can shift part of its transport-energy demand from imported petroleum products to domestically generated electricity.

The macroeconomic logic is clear. The Budget Speech says geopolitical tensions have affected Tanzania through international trade and investment, and that retail prices for petrol and diesel in Dar es Salaam rose by 44 percent and 49 percent, respectively, between March and May 2026. The government responded by monitoring fuel prices, providing diesel subsidies for May and June 2026, and committing in the medium term to accelerate alternative energy investments, including renewable energy, to reduce dependence on imported fuel.

That gives Tanzania’s electric mobility push a harder economic foundation. Electric vehicles are not only a climate story. They are a foreign-exchange story, a fuel-security story and a cost-of-living story. A transport system heavily dependent on imported petrol and diesel is exposed to every oil-price shock, geopolitical tension and currency movement. Electric mobility offers Tanzania a way to move part of that exposure into its domestic power system.

The electricity base has also changed. The Budget Speech says the government spent 1.59 trillion shillings on electricity generation, transmission and distribution projects, including the national grid, and that completion and launch of the Julius Nyerere Hydropower Project, generating 2,115 megawatts, brought national power-generation capacity to 4,522.54 megawatts. It also says 521.3 billion shillings was disbursed through the Rural Energy Agency for rural electrification, enabling 39,003 hamlets to gain access to electricity.

That power-generation base improves the credibility of electric mobility, but it does not automatically solve the charging problem. Charging stations require dependable distribution networks, transformer capacity, safe installations, clear tariffs, digital payment systems, maintenance response and uptime monitoring. In the electric vehicle market, a broken charger can be more damaging than no charger because it destroys confidence.

The Dodoma launch is therefore important not because it solves the market, but because it points toward the next question: can Tanzania build a reliable charging network that follows the country’s real mobility corridors?

Dodoma is not a random location. The Budget Speech frames the capital as a future symbol of economic transformation, a strategic transport and logistics hub serving Tanzania and neighbouring countries, and a model of sustainable urban development. It specifically identifies the Standard Gauge Railway and Msalato International Airport as opportunities to accelerate that vision.

An electric vehicle charging station in Dodoma, therefore, sits inside a larger urban and logistics narrative. A modern capital city cannot be built only on administrative buildings. It needs modern transport systems, cleaner energy use, smarter infrastructure and mobility options that reduce long-term operating costs.

The global market is moving in the same direction. The International Energy Agency says electric car sales exceeded 20 million globally in 2025, growing by 20 percent and accounting for one-quarter of all new cars sold. The agency expects electric car sales to reach 23 million in 2026, representing 28 percent of total car sales. China remains the largest electric vehicle manufacturing hub, while electric vehicles represented nearly 55 percent of all car sales in China and 28 percent in Europe in 2025.

For Tanzania, these numbers do not mean immediate mass adoption. The domestic market is still shaped by imported used vehicles, high upfront-cost sensitivity, fuel-station familiarity, conventional mechanic networks and resale habits built around petrol and diesel vehicles. But the global shift affects Tanzania in several ways. It changes the vehicle supply. It lowers battery and model costs over time. It increases the availability of used electric vehicles. It attracts charging-technology providers. It pushes banks, insurers and dealers to start learning a new asset class.

The International Energy Agency also notes that, in emerging economies with low motorisation and high fuel-price sensitivity, electric two- and three-wheelers can be especially attractive. Sales of electric two- and three-wheelers more than doubled year-on-year in the first quarter of 2026 in Southeast Asia and grew by more than 30 percent in India.

That insight is critical for Tanzania. The first serious wave of electric mobility may not come from private electric cars. It may come from vehicles that move frequently and can justify the economics faster: motorcycles, three-wheelers, taxis, ride-hailing fleets, delivery vans, school transport, government fleets, municipal vehicles, airport transfers and urban buses.

This is where policymakers should avoid the mistake of designing incentives mainly for high-end private electric cars. The better target is high-utilisation transport. A private car may sit idle for most of the day. A taxi, delivery vehicle, motorcycle, bus, or government fleet vehicle moves constantly. That means fuel savings, maintenance savings and predictable charging can be measured more clearly.

The continental policy environment also supports Tanzania’s direction. In April 2026, African transport and energy ministers endorsed a Continental Framework on Electric Mobility at the African Union’s Specialized Technical Committee on Transport and Energy. The framework aims to scale investment in electric vehicles while addressing transport-related air pollution, greenhouse gas emissions, safety and accessibility challenges.

The United Nations Environment Programme has also identified Tanzania among African countries involved in electric mobility work, including electric two- and three-wheelers and zero- and low-emission buses. That reinforces the point that Tanzania’s practical electric mobility opportunity is likely to be strongest in public, shared and high-use transport before it becomes a mass private-car market.

Tanzania’s electric vehicle story should therefore not be read through the Dodoma charging station alone. The stronger reading is that several separate policy, infrastructure and market signals are beginning to converge.

The first related case is the government’s wider power-generation push. A stronger generation base gives Tanzania more room to treat transport electrification as a serious energy-use pathway. The question now shifts from generation to distribution: can Tanzania Electric Supply Company Limited and private operators ensure that charging stations are connected to reliable local networks with enough transformer capacity, safety standards and maintenance support?

The second case is rural electrification. The government’s disbursement through the Rural Energy Agency, enabling 39,003 hamlets to access electricity, adds a long-term national dimension to the electric mobility story. Electric mobility will begin in cities and on major corridors, but Tanzania’s mobility system is not only urban. Motorcycles, three-wheelers, agricultural logistics, rural trade and small transport operators matter across the country. Rural electrification does not immediately create an electric vehicle market, but it expands the future geography where electric motorcycles, small cargo vehicles, battery systems and charging services could operate.

The third case is the value added tax exemption for charging-station equipment. This is one of the clearest signs that the state is willing to sacrifice short-term tax revenue to support early-stage market infrastructure. In a young electric vehicle market, the charging network is the confidence layer. Without it, vehicle adoption remains narrow. By reducing the tax burden on charging equipment, Tanzania is lowering the cost of entry for charging operators, energy companies, malls, petrol-station owners, hotels, public institutions and fleet operators.

The fourth case is the existing tax relief on electric vehicle-related components and systems. The Budget Speech points not only to finished vehicles but also to conversion systems, lithium-ion accumulators, assembly and manufacturing. That matters because the most realistic near-term value chain may not be full electric car manufacturing. It may be assembly, conversion, battery diagnostics, electric motorcycle assembly, charging installation, fleet software, service centres and technician training.

The fifth case is Dodoma’s development as a modern capital and logistics hub. A charging station in Dodoma is not only about one location. It fits into the government’s ambition to make the capital a model of modern, sustainable infrastructure. If Dodoma is meant to become a transport and logistics hub, electric mobility infrastructure becomes part of the city’s future identity, especially for public institutions, airport transfers, government fleets, taxis, delivery services and intercity movement.

The sixth case is Dar es Salaam’s sustainable transport experience. The United Nations Environment Programme has highlighted Dar es Salaam’s transport improvements, including the Bus Rapid Transit system, cycling and walking infrastructure, and pedestrian safety improvements that helped the city win the Sustainable Transport Award in 2018.

This adds an important lesson: Tanzania’s clean mobility story should not be limited to electric cars. The strongest urban mobility systems combine mass transit, walking, cycling, shared mobility and clean vehicle technologies. Electric vehicles can support cleaner transport, but they should complement, not replace, broader urban mobility reform.

The seventh case is the rise of a local electric mobility ecosystem. The Tanzania Electric Mobility Association describes itself as a national platform uniting stakeholders driving electric mobility adoption, with work around capacity building, technical skills, investment, innovation and public adoption of electric vehicles, batteries and charging systems. Its market overview indicates that the country still has fewer than 1,000 registered electric vehicles, limited public charging infrastructure and more than USD 1 million in investment.

This adds realism. Tanzania’s electric mobility market is still small. The country is not yet at mass adoption. But the existence of a national stakeholder platform shows that the sector is beginning to organise itself. Young markets need coordination between government, utilities, vehicle importers, charging operators, financiers, training institutions and users.

The eighth case is the rise of local electric mobility service providers. HASACOM, a Tanzanian electric mobility company, says it began from a charging-access problem encountered through electric bikes used in delivery operations and now supports more than 30 riders using electric two-wheelers and three-wheelers in the city centre.

This adds a practical market lesson. Electric mobility will not grow only through policy documents. It will grow through operational problems being solved: where riders charge, how long they wait, how fleet managers monitor batteries, how delivery riders reduce running costs, and how service providers keep vehicles on the road. These micro-cases show where the economics may first become visible.

The ninth case is the electric three-wheeler model in Dar es Salaam. Urban Electric Mobility Initiative profiles Ziotio UN Limited, operating under the TRī brand, as a Tanzania-based electric mobility company selling smart, connected, zero-emission electric three-wheelers to professional taxi drivers through a lease-to-own model. The initiative says TRī proved product-market fit in Dar es Salaam in 2022, achieved 94 percent of its operational cost targets, built a waiting list of 30 customers and planned to grow its fleet to 250 electric three-wheelers.

This adds a key commercial insight: high-use commercial vehicles are more likely to adopt electric mobility early than ordinary private cars. Three-wheelers, taxis, delivery vehicles, motorcycles and fleet vehicles have daily operating costs that can make electric mobility attractive if charging, servicing and financing are reliable.

The tenth case is the continental electric bus and public transport agenda. The United Nations Environment Programme’s electric bus programme supports countries and cities across Africa, Asia, Latin America and the Caribbean to prepare for low-emission public transport, including electric buses. The programme focuses on reducing urban air pollution and greenhouse-gas emissions from bus fleets while supporting strategies, business models, financing schemes and pilot projects.

This adds a public-transport dimension to Tanzania’s electric vehicle story. If electric mobility is treated only as a private-vehicle technology, the impact will be limited. If it extends to buses, public fleets, shared mobility, and high-use urban transport, the effect on operating costs, air quality, and public visibility could be greater.

The economics, however, remain hard.

The first barrier is upfront cost. Tanzania’s vehicle market is price-sensitive, and many consumers buy used imported vehicles because they are affordable at purchase. Electric vehicles may be cheaper to operate, but if the purchase price remains high, adoption will stay narrow. This is why tax relief on charging infrastructure is useful but incomplete. Vehicle financing, battery warranties, lease structures and residual-value data will matter just as much.

The second barrier is trust. A buyer will ask whether the vehicle can handle Tanzanian roads, heat, dust, floods and long distances. A fleet operator will ask who services the vehicle after the warranty. A bank will ask how to value a used electric vehicle. An insurer will ask how to price battery risk. A driver will ask what happens if the nearest charger fails. These are not anti-innovation questions. They are the normal questions of a market that has seen new technologies arrive before the supporting ecosystem was ready.

The third barrier is grid-readiness at the local level. National generation capacity is one thing; reliable charging at specific locations is another. Fast chargers can create concentrated demand on distribution networks. If Tanzania wants charging corridors, Tanzania Electric Supply Company Limited, charging operators, fuel-station owners, malls, hotels, transport firms and local governments will need coordinated planning around transformers, grid upgrades, solar integration, battery storage and time-of-use tariffs.

The fourth barrier is standards. Tanzania will need clarity on charging connectors, installation safety, charger certification, payment interoperability, tariff setting, battery safety, emergency response, vehicle inspection and recycling. Without standards, the market risks fragmentation: different chargers, different connectors, uneven safety quality and low consumer confidence.

The fifth barrier is skills. Electric vehicles require technicians trained in high-voltage systems, battery diagnostics, power electronics, software, thermal systems and charging infrastructure. Tanzania’s mechanic economy is strong but largely built around internal-combustion engines. The electric vehicle transition will require technical colleges, vocational institutions, dealers, utilities and private operators to build a new skills pipeline.

The opportunity is that these barriers are also investment openings.

Charging stations require electrical contractors, civil works, software, maintenance teams and payment systems. Electric fleets require financiers, insurers, data platforms, fleet managers and service centres. Vehicle imports require inspection and standards. Battery systems require diagnostics, warranties and eventually recycling. Public transport electrification requires depots, route planning and grid coordination. If Tanzania handles the transition properly, electric mobility can create a local services economy around transport electrification.

That is why the government’s tax measure should be seen as a market-making intervention. Exempting charging-station equipment from value added tax reduces the cost of early infrastructure. But the larger policy package must now move from incentive to execution.

The country needs a national charging infrastructure map. It needs priority corridors. It needs public procurement guidelines for electric vehicles. It needs pilot fleets in government, delivery, ride-hailing and urban transport. It needs technical standards. It needs financing models. It needs training programmes. It needs data on charger uptime, energy consumption, vehicle performance and cost per kilometre.

The strongest early strategy would be to electrify where movement is predictable. Government vehicles that operate within cities. Airport transfer fleets. Delivery vehicles returning to depots. School transport with fixed routes. Municipal vehicles. Urban buses with depot charging. Motorcycles and three-wheelers in high-density areas. These segments can prove the economics before the broader consumer market moves.

The traditional fuel-driven market will not disappear quickly. Petrol and diesel vehicles still have overwhelming advantages: fuel stations everywhere, known repair networks, familiar import channels, established resale markets and lower upfront prices for used vehicles. Hybrids may also grow as a bridge technology for consumers not yet ready for full electric vehicles.

But transitions do not begin when the old system disappears. They begin when the new system becomes credible.

The Dodoma charging station is therefore not the end of anything. It is the beginning of a test. Can Tanzania turn an electric vehicle charging point into a network? Can it turn a tax exemption into investment? Can it turn power-generation gains into lower transport costs? Can it turn clean mobility into a local services industry? Can it make electric mobility practical for fleets before asking ordinary consumers to follow?

If the answer is yes, Tanzania’s mobility landscape will change gradually but materially. The first signs will not be mass private electric car ownership. They will be government fleets, taxis, delivery vehicles, motorcycles, buses and corridor chargers. They will be technicians trained to service electric systems. They will be banks offering electric vehicle financing. They will be public institutions measuring operating-cost savings. They will be charging stations that work reliably.

Tanzania’s electric mobility story is being built one charging station at a time. But the real story is bigger than the station. It is about whether the country can use fiscal policy, electricity infrastructure, urban planning, private-sector experimentation and fleet economics to begin shifting a fuel-driven transport market toward a more resilient model.

In a petrol-and-diesel market, electric vehicles will not win because they are fashionable. They will win only when they become practical, affordable, serviceable and reliable.

Dodoma is a start. The market will decide whether it becomes a turning point.

Uchumi360

Business Intelligence

Uchumi360

Business Intelligence

Uchumi360 covers business, investment, and economic policy across East, Central, and Southern Africa.

For the serious reader

You read to the end. That places you in a small group.

Uchumi360 is built for readers who demand precision over speed, structure over sentiment, and analysis that holds uncomfortable conclusions rather than softening them. If this work sharpens how you think about Africa's economy, help us keep building the infrastructure behind it.

Institutional Partners

Commission intelligence. Shape the conversation.

Uchumi360 works with development finance institutions, investment firms, sovereign bodies, and strategic organisations across the coverage region. Institutional partnership unlocks:

- Commissioned sector and country intelligence reports

- Branded research series under your institution's authority

- Exclusive data briefings for internal strategy teams

- Speaking and editorial presence at Uchumi360 events

- Co-published investment outlooks for your markets

Support Our Work

Independent analysis has a cost. Help us bear it.

Uchumi360 does not carry advertising. It does not take editorial direction from sponsors. Every article is produced without commercial compromise. Your contribution funds the reporting, research, and editorial infrastructure that keeps this analysis free from influence.

Secure checkout: One-time and monthly support are processed securely. Add payment credentials to enable checkout here.

Stay Connected

Keep up with every new insight.

Follow our latest analysis, policy coverage, and market intelligence as soon as it is published. If you need something specific, reach out directly and we will point you to the right research.