Tanzania’s Uranium Window: The Numbers Behind Mkuju River’s Investment Case

Ready

The project’s current resource base is sizeable by regional standards. The 2024 Red Book figures cited by the World Nuclear Association measure Mkuju River’s identified in-situ uranium resources at about 72,200 tonnes of uranium, with reasonably assured recoverable resources of about 40,400 tonnes at up to USD 130 per kilogram of uranium.

Tanzania’s uranium story is beginning to move from a long-delayed mining file into a more serious investment conversation. The reason is not only that the country has uranium underground, but that the global uranium cycle has changed at the same time that the Mkuju River Uranium Project has returned to a more active development path.

For investors, that combination matters. Uranium is not a normal mineral. It is tied to nuclear fuel, long-term energy security, geopolitics, environmental risk, export controls and highly specialised regulation. A uranium project can have a large resource base and still fail to become bankable if the price, financing, licence tenure, processing route, water management, community acceptance and regulatory framework are not aligned.

That is why Mkuju River should not be read as a simple mining story. It is better understood as a strategic-minerals investment case whose numbers are becoming too important to ignore, but whose risks remain too serious to underprice.

The global market is the first part of the thesis. The World Nuclear Association’s 2025 fuel outlook projects global nuclear generating capacity rising from about 398 GWe in 2025 to 746 GWe by 2040 in its reference scenario. That matters because reactor growth feeds directly into uranium demand. The same outlook estimates global reactor uranium requirements at about 68,920 tonnes of uranium in 2025, rising to just over 150,000 tonnes by 2040 in the reference case, and above 204,000 tonnes in the upper scenario.

Those figures are the macro signal behind Tanzania’s opportunity. The world does not simply need more nuclear ambition; it needs fuel supply to match that ambition. New uranium mines take time to finance, permit, build and bring into steady production. Existing mines face depletion pressures. Utilities prefer supply certainty. Governments are increasingly sensitive to where strategic fuels come from. That environment gives credible uranium projects more strategic value than they had during the weak post-Fukushima pricing cycle.

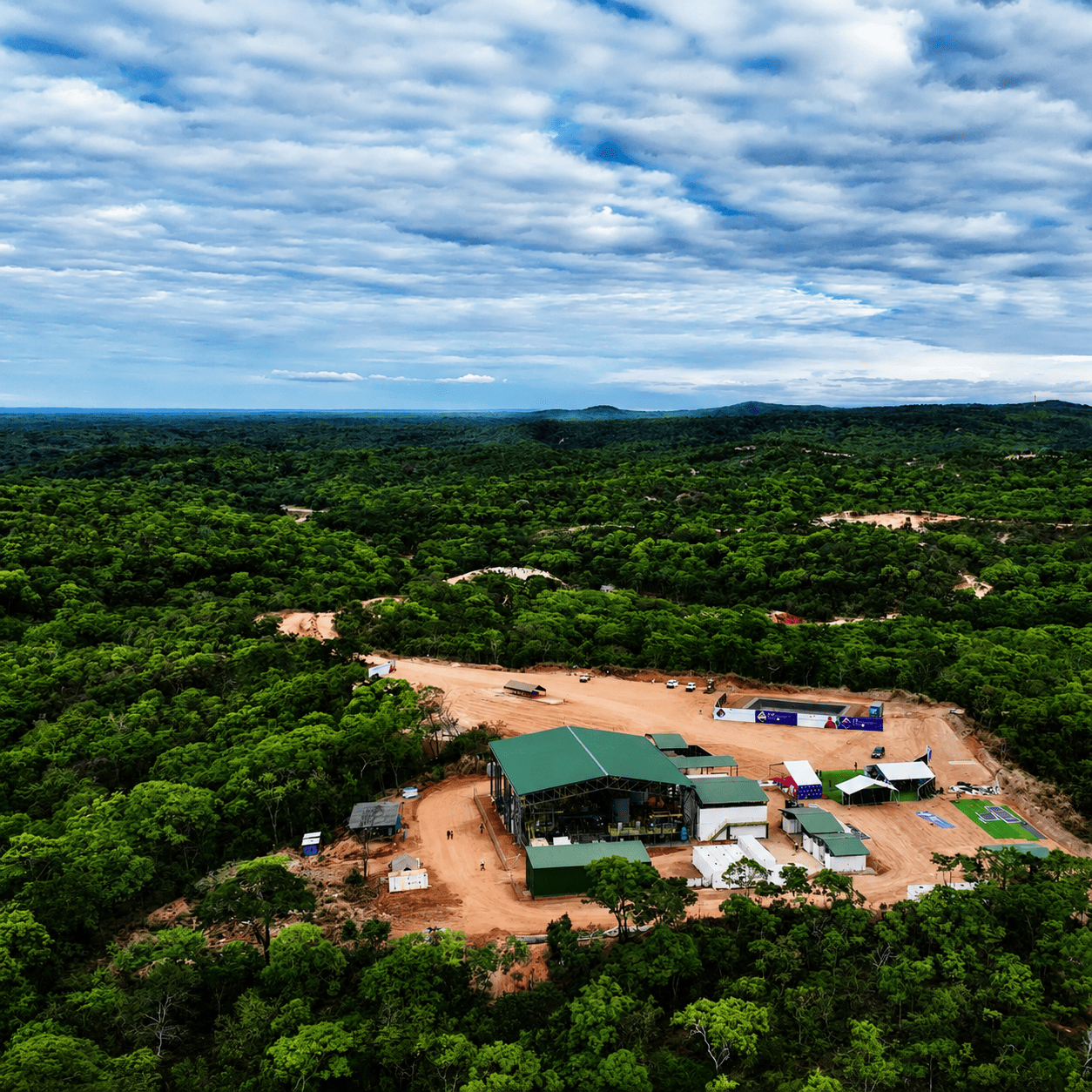

Mkuju River is Tanzania’s anchor uranium asset. The project incorporates the Nyota deposit in Namtumbo District, Ruvuma Region, about 470 kilometres southwest of Dar es Salaam. It is operated by Mantra Tanzania Limited, part of Uranium One Group, which is linked to Russia’s Rosatom nuclear ecosystem. The project received a Special Mining Licence in April 2013, but development slowed after uranium prices weakened.

The project’s current resource base is sizeable by regional standards. The 2024 Red Book figures cited by the World Nuclear Association measure Mkuju River’s identified in-situ uranium resources at about 72,200 tonnes of uranium, with reasonably assured recoverable resources of about 40,400 tonnes at up to USD 130 per kilogram of uranium. Older public summaries also describe the mine as holding an estimated 182.1 million tonnes of ore grading 0.025% uranium. These figures are not interchangeable, because ore tonnage, grade, in-situ resources and recoverable resources describe different things. Still, they point to the same conclusion: Mkuju River is not a marginal uranium occurrence. It is a large project with the potential to place Tanzania on the uranium supply map.

The production plan is what turns the resource into an investment story. In July 2025, a pilot uranium processing plant was commissioned at the Nyota deposit. The pilot plant is designed to test uranium processing technologies and generate data for the main processing complex. Public industry reporting states that the future main complex is planned to have production capacity of up to 3,000 tonnes of uranium per year, with construction scheduled to begin in the first quarter of 2026 and commissioning targeted for 2029.

The commercial scale is material. Three thousand tonnes of uranium per year is broadly equivalent to about 7.8 million pounds of U3O8. Using Cameco’s published June 2026 spot price of USD 85.00 per pound, that implies a notional annual gross sales scale of about USD 663 million before production costs, recoveries, taxes, royalties, financing, transport, offtake pricing, state participation and operating risk. This is not a revenue forecast. It is a scale estimate to show the size of the opportunity if the planned capacity is achieved.

The price environment is also stronger than it was during the period that delayed the project. Cameco’s published market table shows uranium spot prices at USD 85.00 per pound in June 2026, while the long-term uranium price stood at USD 95.50 per pound. That difference is important because uranium projects are often financed around long-term contracting logic, not only spot-market enthusiasm. For a mine that needs large upfront capital and long payback periods, long-term price signals matter.

The historical cost figures suggest why the market cycle matters so much. World Nuclear Association data cite older capital-cost estimates of about USD 430 million for the treatment plant and infrastructure, a conventional mining cash cost of about USD 25 per pound U3O8, and overall costs above USD 50 per pound. These figures should not be treated as current feasibility numbers, because inflation, engineering changes, water systems, security, financing costs, environmental controls and processing choices may have changed the economics. But they provide a useful reference point: a project that was unattractive in a weak uranium market can look different when spot and long-term prices move materially higher.

The investment case is also supported by local economic numbers. Tanzania’s Ministry of Minerals has reported that Mantra is seeking capital for the mine and the main processing plant, and that discussions involve Russian financial institutions as well as Tanzanian banks including CRDB and NMB. The same ministry reporting says the project is expected to create more than 4,000 direct jobs for residents of Namtumbo and nearby areas, while more than 21,000 households are expected to benefit through the project value chain.

Those figures should be handled carefully. Job numbers in large mining projects often combine construction-phase and operating-phase expectations. Household-benefit numbers depend on how the value chain is structured. Investors should therefore treat the 4,000-job and 21,000-household figures not as guaranteed outcomes, but as measurable commitments that need procurement plans, training systems, supplier-development programmes, community agreements and transparent reporting.

The licence issue is one of the most important numbers in the whole investment thesis. The Ministry of Minerals has reported that Mantra’s leadership identified the expected expiry of the mining licence in April 2028 as a challenge for securing long-term loans. This is a bankability issue. A uranium project with a main processing complex, construction risk and long-term repayment needs cannot be financed comfortably if lenders are uncertain about licence tenure beyond the construction and payback horizon.

For Tanzania, this creates a policy task. The government needs to provide enough licence certainty to unlock long-term capital while maintaining strong regulatory discipline. Investors need predictability, but the public also needs safeguards. In a sensitive uranium project, those two objectives should reinforce each other rather than compete.

The environmental numbers also matter. World Nuclear Association reporting notes that the government allocated 345 square kilometres of land inside the 50,000-square-kilometre Selous Game Reserve to the project, equivalent to about 0.7% of the reserve’s area. Uranium Network records that in 2012 the World Heritage Committee accepted a boundary change to allow uranium exploitation south of the World Heritage Site, in the Selous-Niassa Wildlife Corridor, and that the Selous Game Reserve was placed on the endangered World Heritage list in 2014.

That conservation history will remain part of the project’s risk profile. Even if the project has legal approvals, investors should assume that biodiversity, water, tailings, radiation safety, transport and rehabilitation will remain under scrutiny. Environmental credibility is not a public-relations add-on here; it is central to bankability.

Water risk deserves special attention. World Nuclear Association data indicate that the project’s resources are extensive, sandstone-hosted and shallow, with present plans involving multiple pits feeding a single mill using conventional acid leach and resin-in-pulp recovery. It also notes that in-situ leach mining using acid may be employed, especially for the 13% of resources outside designed pits and also below the water table, while about one-third of the total resource is below the water table. This is a major due-diligence point because water and groundwater protection can affect permitting, processing design, environmental trust and financing.

The Geological Survey of Tanzania adds another part of the investment infrastructure. GST identifies uranium among the minerals that are part of current exploration activity in Tanzania, alongside gold, base metals, platinum group metals, gemstones, diamonds and industrial minerals. GST also states that Tanzania has strong geological databases, infrastructure, mineral policy conditions and accessible exploration services, and that it provides specialist services to exploration and mining companies, including geological, geochemical and geophysical work, mineral evaluation and project assessment.

For investors, this matters because uranium investment depends on quality data. The asset is not only judged by headline resource size. It is judged by geology, hydrology, environmental baseline, radiometric data, processing behaviour, monitoring systems and rehabilitation assumptions. The stronger the country’s geoscience base, the easier it becomes to price risk.

The geopolitical layer cannot be ignored. Mantra Tanzania’s ownership link to Uranium One and Rosatom gives the project access to a serious nuclear-sector ecosystem, but it also introduces political and financial complexity. Russia-linked assets face additional scrutiny in parts of the global financial system, and investors must consider sanctions exposure, banking channels, offtake markets, technology dependence and diplomatic risk. This does not make the project uninvestable, but it changes how capital should price the opportunity.

The most realistic investor view is therefore neither excitement nor dismissal. Mkuju River is now in the serious due-diligence zone. The numbers justify attention: 72,200 tonnes of identified in-situ uranium resources, 40,400 tonnes of reasonably assured recoverable resources, a planned 3,000-tonne-per-year production complex, an estimated notional gross sales scale above USD 660 million per year at June 2026 spot prices, more than 4,000 expected direct jobs, more than 21,000 households linked to value-chain benefits, and a global market where uranium demand could more than double by 2040.

But the risks are just as clear. The April 2028 licence-tenure issue must be resolved. Updated capex and opex need to be verified. Pilot plant results must support commercial processing assumptions. Water and environmental controls must be credible. Community benefits must be structured. Financing must move from discussion to commitment. The geopolitical structure must be understood. Offtake arrangements must become clearer.

For local investors and service providers, the opportunity is not limited to mine ownership. Mkuju River could create demand for construction, logistics, security, camp services, engineering, environmental monitoring, laboratory services, worker housing, medical support, food supply, transport, professional services and supplier finance. The value chain may become the more accessible opportunity for Tanzanian businesses.

For banks, the opportunity is project-linked finance. Local institutions may participate through supplier finance, contractor finance, equipment finance, working capital, payroll banking and guarantees, even if the core project debt comes from larger foreign or strategic financiers.

For government, the opportunity is bigger than royalties. Uranium can help Tanzania position itself as a strategic-minerals jurisdiction with gold, graphite, nickel, rare earth potential, gas, ports, special economic zones and industrial corridors. If managed well, it can also strengthen national capacity in radioactive ore regulation, geoscience, environmental monitoring, laboratory services, radiation safety and nuclear-sector governance.

The bottom line is that Tanzania’s uranium window is opening, but it is not yet fully de-risked. The market supports renewed attention. The resource base is material. The pilot plant is a meaningful technical step. Government support is visible. The local economic promise is large. But licence certainty, financing, ESG credibility, processing performance and geopolitical risk will determine whether Mkuju River becomes a bankable uranium mine or remains a strategic possibility.

That is precisely why investors should study it now. The opportunity is real, but the premium will go to those who understand the numbers before the headline becomes obvious.

Uchumi360

Business Intelligence

Uchumi360

Business Intelligence

Uchumi360 covers business, investment, and economic policy across East, Central, and Southern Africa.

For the serious reader

You read to the end. That places you in a small group.

Uchumi360 is built for readers who demand precision over speed, structure over sentiment, and analysis that holds uncomfortable conclusions rather than softening them. If this work sharpens how you think about Africa's economy, help us keep building the infrastructure behind it.

Institutional Partners

Commission intelligence. Shape the conversation.

Uchumi360 works with development finance institutions, investment firms, sovereign bodies, and strategic organisations across the coverage region. Institutional partnership unlocks:

- Commissioned sector and country intelligence reports

- Branded research series under your institution's authority

- Exclusive data briefings for internal strategy teams

- Speaking and editorial presence at Uchumi360 events

- Co-published investment outlooks for your markets

Support Our Work

Independent analysis has a cost. Help us bear it.

Uchumi360 does not carry advertising. It does not take editorial direction from sponsors. Every article is produced without commercial compromise. Your contribution funds the reporting, research, and editorial infrastructure that keeps this analysis free from influence.

Secure checkout: One-time and monthly support are processed securely. Add payment credentials to enable checkout here.

Stay Connected

Keep up with every new insight.

Follow our latest analysis, policy coverage, and market intelligence as soon as it is published. If you need something specific, reach out directly and we will point you to the right research.