Ugandan Supermarkets Are Exposing East Africa’s Regional Trade Imbalance

Ready

This is not an argument against imports. Every growing economy imports. The strategic question is different: what is Uganda importing, from where, and why are East African producers not filling more of those shelves?

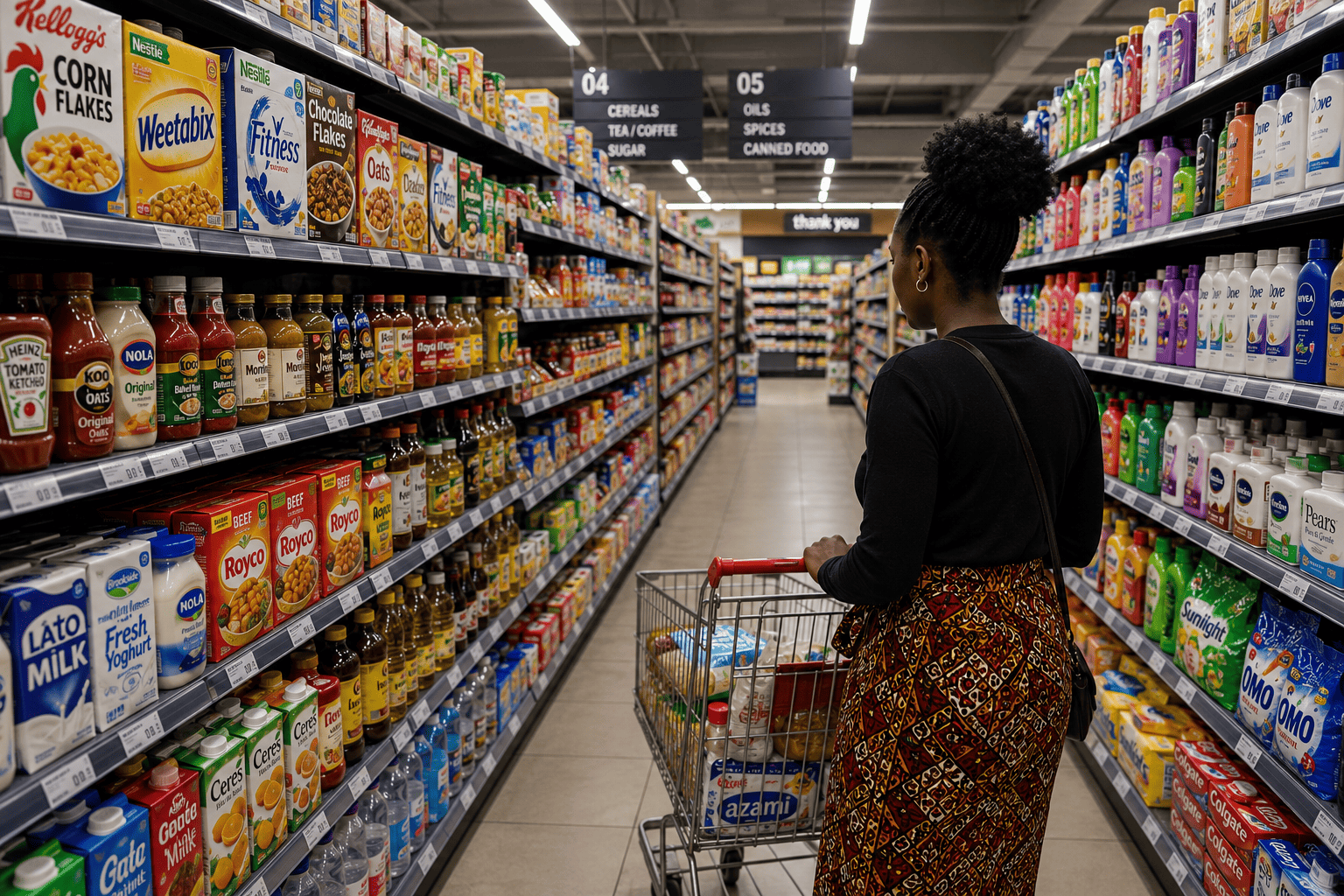

Walk into a supermarket in Kampala and the shelves tell a more honest story than most regional trade speeches. Cereals, sauces, biscuits, juices, cosmetics, detergents, skin-care products, baby-care goods, packaged foods and household items reveal a simple but uncomfortable truth: Uganda sits inside the East African Community, but a large part of its consumer economy is still supplied by countries outside the region.

This is not an argument against imports. Every growing economy imports. The strategic question is different: what is Uganda importing, from where, and why are East African producers not filling more of those shelves?

The most recent official data gives the argument a sharper edge. Uganda’s Ministry of Finance, Planning and Economic Development reported that merchandise imports grew by 47.3%, from USD 1.049 billion in July 2024 to USD 1.545 billion in July 2025. The increase was driven by formal private-sector imports, including mineral products, machinery equipment, vehicles and accessories, petroleum products, prepared foodstuffs, beverages and tobacco. Month-on-month, imports also rose by 8.3%, from USD 1.427 billion in June 2025 to USD 1.545 billion in July 2025.

The origin of those imports is the real story. In July 2025, Asia was Uganda’s largest import source, accounting for 35.6% of the country’s total import bill. Within Asia, China, India and Japan were the dominant suppliers, accounting for 55.5%, 22.0% and 9.0% of Uganda’s Asian import bill respectively. The East African Community supplied 27.0%, the rest of Africa supplied 20.3%, and the European Union supplied 7.2%. Within the East African Community, Tanzania and Kenya accounted for 98.1% of Uganda’s imports from the regional bloc.

That means the East African Community is relevant to Uganda’s import economy, but still narrow. Uganda is not importing evenly from the region. It is importing mainly from Tanzania and Kenya, while China, India, Japan, the United Arab Emirates, Saudi Arabia, Egypt, Turkey, Europe and other external suppliers continue to serve large parts of the formal consumer and industrial market.

The longer customs series confirms that this is not a one-month anomaly. The Uganda Bureau of Statistics’ latest annual statistical abstract shows that Uganda’s formal imports rose from USD 7.70 billion in 2019 to USD 11.78 billion in 2023. Formal and informal imports combined increased from USD 7.75 billion in 2019 to USD 11.90 billion in 2023. That is a five-year increase of more than USD 4 billion in Uganda’s import economy.

The World Bank’s World Integrated Trade Solution database, whose latest Uganda trade summary uses 2023 data, shows the same external dependence. Uganda’s top import partners for all products in 2023 were China, the United Arab Emirates, Tanzania, India and Kenya. China supplied USD 2.294 billion, the United Arab Emirates USD 1.431 billion, Tanzania USD 1.331 billion, India USD 1.256 billion and Kenya USD 824 million. Only two of the top five suppliers were East African Community countries.

The consumer-goods picture is even more revealing. The same World Bank trade database shows that consumer goods accounted for USD 4.759 billion of Uganda’s imports in 2023, representing 40.4% of total imports. Intermediate goods accounted for USD 4.362 billion, or 37.0%. This matters because supermarket shelves are mostly the visible end of the consumer-goods economy. Uganda is not merely importing capital equipment or fuel; it is importing large volumes of finished and semi-finished consumption.

That is why the supermarket shelf has become an economic microscope.

A bottle of imported juice is not just a bottle of juice. It points to gaps in fruit processing, packaging, cold-chain logistics and brand financing. Imported biscuits point to grain processing, baking technology, packaging and shelf-life capability. Imported detergent points to chemical manufacturing and retail packaging gaps. Imported skin-care products point to formulation, certification, consumer trust and beauty-industry industrialisation. Imported cereals point to grain storage, milling, food science and urban retail positioning.

The irony is that Uganda and its neighbours are not short of agricultural potential. Uganda has fertile land and a strong food base. Tanzania has scale and agricultural depth. Kenya has the region’s strongest manufacturing base. Rwanda has administrative discipline and premium branding potential. Burundi and the eastern Democratic Republic of Congo have underdeveloped but relevant agricultural and consumer markets. Yet the regional supermarket economy is still not supplied deeply enough by the region itself.

The East African Community’s own trade statistics underline the wider imbalance. The bloc’s intra-regional trade grew by 28.0% in 2025, reaching USD 19.3 billion, but it accounted for only 12.3% of total trade. The region’s total trade with Africa reached USD 39 billion, accounting for 25.2% of total trade. That is progress, but it also shows how much of the region’s trade still happens outside the region.

The structure of that trade is more troubling. The East African Community’s export profile remained dominated by minerals in 2025. Copper accounted for 39.2% of total exports, while precious metals and stones accounted for 19.5%. Meanwhile, the region continued to import energy, machinery and manufactured goods. In other words, East Africa is still exporting too much raw and semi-processed value while importing too much finished value.

Uganda’s July 2025 import report gives a current snapshot of the same problem. The import categories that grew included prepared foodstuffs, beverages, tobacco, chemical and related products, vegetable products, plastics, rubber and related products. These are not distant industrial categories with no regional production relevance. Several of them are exactly where East Africa should be building stronger consumer-goods, agro-processing and light-manufacturing capacity.

The product-level data makes the argument harder to dismiss. Uganda is not only importing fuel, machinery and vehicles. It is also importing large volumes of consumer-facing and retail-adjacent goods that East Africa could reasonably produce, process, package or supply more competitively.

The clearest example is food. Uganda’s formal imports of cereals and cereal preparations rose from USD 291.7 million in 2019 to USD 443.5 million in 2023, after peaking at USD 479.5 million in 2021 and remaining high at USD 475.0 million in 2022. Cereals are not advanced technology. They are one of the most basic food-economy categories. For a region with Uganda, Tanzania, Kenya, Rwanda, Burundi and eastern Democratic Republic of Congo, this should be a warning sign about grain storage, milling, food processing, breakfast cereal production, fortified foods, packaging and retail distribution.

The same pattern appears in miscellaneous edible products and preparations, a category that captures many supermarket-style processed food items. Uganda imported USD 53.4 million of these products in 2019, rising to USD 85.3 million in 2023. This is the category where urban diets, convenience foods, flavourings, food mixes and processed preparations become visible in customs data. Its growth shows that Uganda’s demand for processed food is expanding, but the region has not yet converted enough of that demand into East African manufacturing.

The dairy line is smaller but symbolically important. Uganda’s formal imports of dairy products and bird’s eggs rose from USD 4.9 million in 2019 to USD 9.2 million in 2023, after reaching USD 9.8 million in 2021. Uganda and its neighbours have livestock, milk production and dairy potential, but supermarket competitiveness depends on more than raw milk. It requires cold chains, pasteurisation, shelf-stable packaging, quality assurance, retail branding and distribution discipline.

Household and personal-care products tell an even stronger story. Uganda’s imports of essential oils, perfume materials, toilet preparations and cleaning preparations increased from USD 119.6 million in 2019 to USD 187.3 million in 2023. This is the supermarket aisle of soaps, detergents, cosmetics, fragrances, toiletries and household cleaners. These are exactly the kinds of light-manufacturing products that regional producers should be scaling, especially because East Africa has oils, botanicals, packaging demand, young consumers and growing urban households.

Packaging is the hidden infrastructure behind all of these shelves. Uganda imported USD 422.7 million of plastics in primary forms in 2023, compared with USD 278.3 million in 2019. Imports of plastics in non-primary forms also rose from USD 46.0 million in 2019 to USD 66.1 million in 2023. Without affordable, good-quality packaging, local and regional producers cannot compete with imported foods, detergents, cosmetics, pharmaceuticals or household goods. Packaging affects shelf life, hygiene, labelling, barcoding, export readiness and consumer trust.

Pharmaceuticals also show the limits of regional industrial depth. Uganda’s formal imports of medical and pharmaceutical products rose from USD 306.3 million in 2019 to USD 534.2 million in 2023, after peaking at USD 578.4 million in 2022. Some of this is necessary because specialised medicines and public-health supplies cannot all be produced locally. But the scale of the import bill still exposes a regional opportunity in basic medicines, medical consumables, packaging, distribution and selected health manufacturing.

The most recent monthly data confirms that the pattern has not disappeared. In June 2025, Uganda’s merchandise imports reached USD 1.427 billion, a 50.7% increase from USD 947.4 million in June 2024. The Ministry of Finance, Planning and Economic Development said the increase was driven by formal private-sector oil and non-oil imports, including vegetable products, animal products, beverages, fats and oils, mineral products, base metals and related products. Month-on-month, imports grew from USD 1.312 billion in May 2025 to USD 1.427 billion in June 2025, with increases in animal products, prepared foodstuffs, beverages and tobacco, chemical and related products, petroleum products and electricity.

The origin data strengthens the regional imbalance argument. In June 2025, the East African Community became Uganda’s largest import source for that month, accounting for 34.8% of total imports, while Asia accounted for 30.7%, the rest of Africa 15.9%, the Middle East 11.6%, and the European Union 3.9%. That monthly shift shows that regional supply can matter. But it also shows how competitive Asia and the Middle East remain in Uganda’s import economy, especially across formal private-sector imports and manufactured goods.

Uganda’s supermarket shelves are not merely filled with foreign goods because consumers prefer foreign brands. They are filled that way because East Africa has not yet built enough regional capacity in the product categories that define daily consumption: cereals, processed foods, dairy products, detergents, cosmetics, packaging, pharmaceuticals, plastics and household goods.

The issue is not that every imported item should be replaced. That would be unrealistic. The issue is that many of these categories are not beyond East Africa’s productive ability. They are not aircraft engines or semiconductor chips. They are food, packaging, cleaning products, personal care, basic pharmaceuticals and processed consumer goods. If the region cannot compete more strongly in these categories, then its integration project remains shallow.

Kenya is the regional exception in several categories. It has the manufacturing base, distribution networks and brands to compete in Uganda. Tanzania is also important, especially in commodity and industrial supply lines. But the rest of the region remains too shallow in formal retail supply. Uganda itself has demand and raw materials, but not enough scaled manufacturers. Rwanda has quality positioning but limited domestic scale. Burundi and the eastern Democratic Republic of Congo remain weak formal suppliers, despite their geographic relevance.

The problem is not consumer disloyalty. Ugandan consumers do not owe local producers loyalty when imported products are cheaper, better packaged, more consistent or more available. Supermarkets also do not owe domestic producers shelf space out of sentiment. Retail is a hard business. Products must arrive on time, meet standards, carry barcodes, offer acceptable margins, survive storage, look credible, and move quickly.

That is where East Africa’s industrial weakness becomes visible. The region has trade protocols, but not enough trade architecture. It has farmers, but not enough processors. It has borders, but not enough efficient corridors. It has small manufacturers, but not enough medium-sized consumer-goods champions. It has policy ambition, but not enough packaging capacity, product testing, certification, working capital and modern distribution.

Uganda should therefore use its import data as an industrial targeting tool. The country should not try to produce everything locally. That would be inefficient and unrealistic. But it should identify the consumer categories where imports are rising, local raw materials exist, production technology is accessible, and regional demand is large enough to justify investment.

The most obvious categories are processed foods, cereals, sauces, juices, dairy products, edible oils, animal feed, detergents, cosmetics, packaging materials, selected pharmaceuticals, household plastics and affordable personal-care goods. These are not glamorous sectors, but they are exactly the sectors that create factories, suppliers, distributors, warehouse jobs, brand owners and exportable regional companies.

The policy response should be practical. Uganda needs cheaper and more reliable industrial energy, stronger packaging capacity, better food-testing laboratories, affordable working capital for manufacturers, supplier-development programmes with supermarkets, and faster standards recognition across the East African Community. A product certified in Kampala should not face unnecessary friction in Nairobi, Kigali, Dar es Salaam, Bujumbura or Goma if the region is serious about integration.

Supermarkets and large retailers should also become part of industrial policy without being forced into uneconomic procurement. They can publish supplier-readiness criteria, share demand data, create trial shelves for certified local and regional brands, support packaging improvement, and build procurement pathways that allow serious small and medium-sized manufacturers to graduate into national supply contracts.

The regional lesson is bigger than Uganda. The East African Community cannot measure integration only by presidential summits, tariff schedules or secretariat reports. It must measure integration by what ordinary consumers buy in Kampala, Kigali, Nairobi, Dar es Salaam, Bujumbura and Goma.

If the shelves are dominated by goods from Dubai, Guangzhou, Mumbai, Cairo, Istanbul, Rotterdam and Riyadh in categories that East Africa can reasonably produce, then the region has not industrialised deeply enough. If the shelves begin to carry more competitive Ugandan, Kenyan, Tanzanian, Rwandan, Burundian and Congolese brands, then East Africa will have moved from treaty integration to production integration.

Uganda is not merely importing products. It is importing the industrial capacity that East Africa has not yet built.

The next phase of regional integration will not be judged in conference halls. It will be judged in supermarket aisles.

Uchumi360

Business Intelligence

Uchumi360

Business Intelligence

Uchumi360 covers business, investment, and economic policy across East, Central, and Southern Africa.

For the serious reader

You read to the end. That places you in a small group.

Uchumi360 is built for readers who demand precision over speed, structure over sentiment, and analysis that holds uncomfortable conclusions rather than softening them. If this work sharpens how you think about Africa's economy, help us keep building the infrastructure behind it.

Institutional Partners

Commission intelligence. Shape the conversation.

Uchumi360 works with development finance institutions, investment firms, sovereign bodies, and strategic organisations across the coverage region. Institutional partnership unlocks:

- Commissioned sector and country intelligence reports

- Branded research series under your institution's authority

- Exclusive data briefings for internal strategy teams

- Speaking and editorial presence at Uchumi360 events

- Co-published investment outlooks for your markets

Support Our Work

Independent analysis has a cost. Help us bear it.

Uchumi360 does not carry advertising. It does not take editorial direction from sponsors. Every article is produced without commercial compromise. Your contribution funds the reporting, research, and editorial infrastructure that keeps this analysis free from influence.

Secure checkout: One-time and monthly support are processed securely. Add payment credentials to enable checkout here.

Stay Connected

Keep up with every new insight.

Follow our latest analysis, policy coverage, and market intelligence as soon as it is published. If you need something specific, reach out directly and we will point you to the right research.