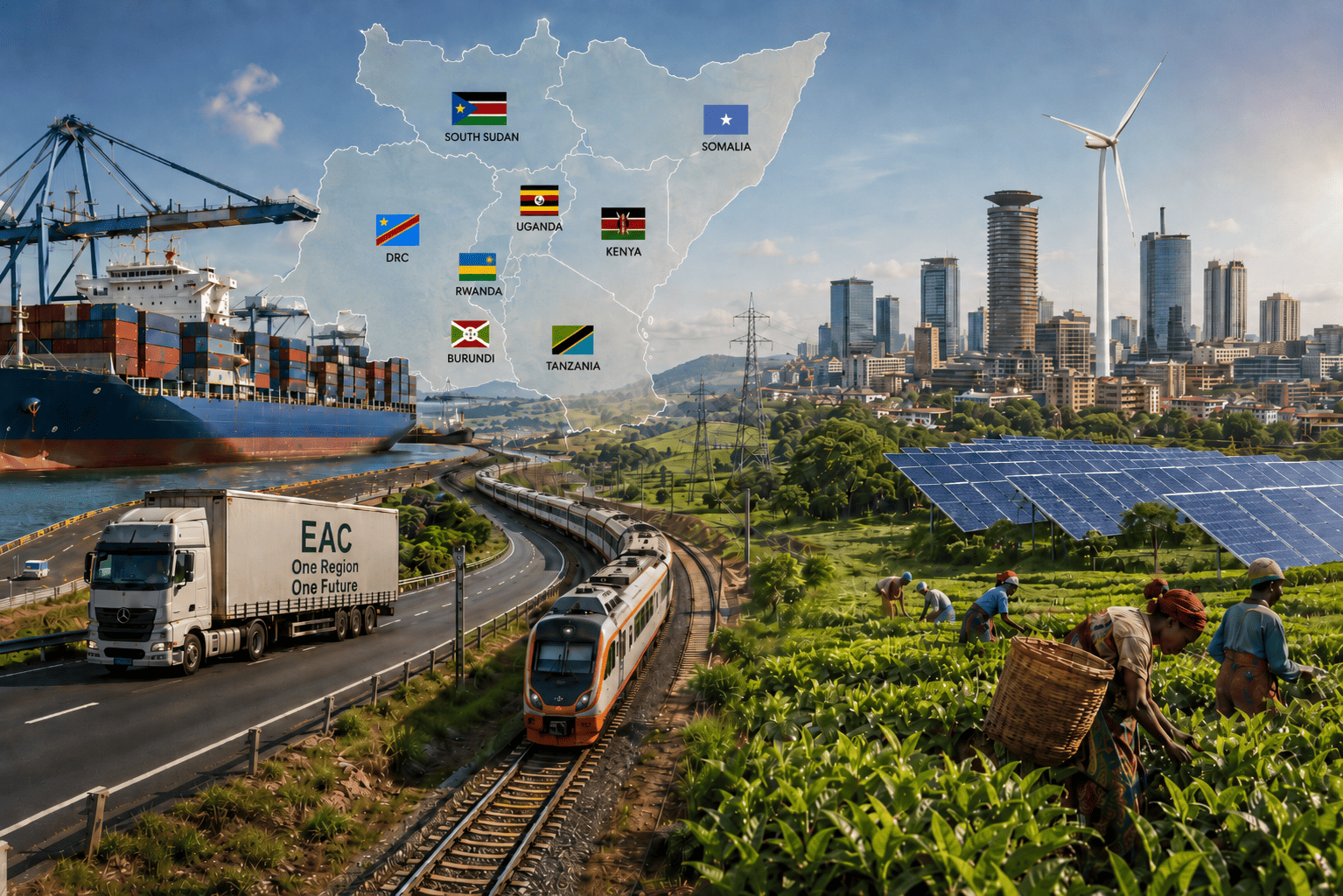

East Africa’s Next Growth Story Depends on Turning Eight National Visions Into One Market

Ready

Tanzania is the logistics-industrial anchor. Kenya is the services and capital market hub. Uganda is the agro-energy hinge. Rwanda is the execution state. Burundi is an equity and state-renewal economy. Somalia is the maritime frontier. South Sudan is the peace-first resource frontier. DRC is the continental-scale mineral and market multiplier. The EAC’s challenge is to make those roles work as one regional system.

Across the eight-member East African Community, governments have drawn up long-term blueprints that read less like aid-era poverty plans and more like economic prospectuses. Tanzania aims to become a $1 trillion upper-middle-income economy by 2050. Kenya wants to be a globally competitive, newly industrialising economy by 2030. Uganda’s Vision 2040 seeks to move the country from a peasant society to a modern and prosperous upper-middle-income state. Rwanda is targeting upper-middle-income status by 2035 and high-income status by 2050.

Burundi wants to become an emerging economy by 2040 and a developed economy by 2060. Somalia is using its National Transformation Plan to rebuild governance and push economic normalisation. South Sudan’s development logic remains anchored in peace, state building and diversification. The Democratic Republic of Congo, the bloc’s largest geographic and resource frontier, is working through a strategic plan focused on governance, diversification, human capital, infrastructure and balanced provincial growth.

Individually, these are national plans. Collectively, they form the outline of a regional growth thesis: East Africa wants to move from fragmented markets, commodity dependence and infrastructure bottlenecks toward a connected production economy built on corridors, ports, power, minerals, digital systems, agriculture, services, industry and a young labour force.

The missing link is execution across borders.

That is where the region’s national visions converge. Strip away the different dates, political language and country-specific priorities, and the same core pillars appear repeatedly: infrastructure and corridors, industrialisation and value addition, agriculture and food security, energy security, human capital, digital transformation, governance and peace, climate resilience, trade integration, private-sector growth, productive cities, natural-resource management, youth employment, and implementation discipline.

These are not abstract planning themes. They are the economic mechanics of whether East Africa can become a serious regional production system.

Infrastructure and corridors are the first convergence area. Tanzania, Kenya, Uganda, Rwanda, Burundi, Somalia, South Sudan and DRC all treat roads, ports, railways, border posts, airports, energy lines and digital networks as the backbone of transformation. For coastal countries such as Tanzania, Kenya and Somalia, infrastructure is about ports and maritime gateways. For land-linked economies such as Rwanda, Uganda, Burundi, South Sudan and DRC, it is about reducing the cost of distance. Under the EAC, this becomes a corridor agenda: the region cannot industrialise if goods remain trapped by poor roads, slow customs, expensive logistics and weak cross-border systems.

Tanzania is the region’s logistics-industrial anchor. Its Dira 2050 is built around a strong, inclusive and competitive economy; human capabilities and social development; and environmental integrity and climate resilience. The plan’s strategic drivers, integrated logistics, energy, science and technology, research and development, and digital transformation, make Tanzania more than a national growth story. They position it as one of the EAC’s main operating platforms.

That role is geographic as much as political. Dar es Salaam, Tanga and Mtwara give Tanzania maritime weight. The central corridor gives it access to Rwanda, Burundi, Uganda and eastern DRC. Its energy potential, mining base, agricultural land, tourism assets and industrial ambitions give it the ingredients of a regional production state. If Dira 2050 works, Tanzania becomes not only richer, but more central to how the EAC moves goods, power, people and capital.

Kenya is the region’s services and capital-market hub. Vision 2030 rests on economic, social and political pillars, backed by infrastructure, macroeconomic stability, science, technology and innovation, land reforms, human-resource development, security and public-sector reforms. Its advantage is not one sector. It is ecosystem depth.

Nairobi already operates as East Africa’s boardroom. Finance, insurance, logistics, technology, media, diplomacy, aviation, professional services and development institutions cluster there. Mombasa remains a critical gateway for Uganda, Rwanda, Burundi, South Sudan and eastern DRC. Kenya’s long-term regional value will depend on whether it uses that lead to dominate neighbouring markets or to help build deeper regional value chains. The former creates resentment. The latter creates scale.

Uganda is the agro-energy hinge. Its Vision 2040 identifies oil and gas, tourism, minerals, ICT, labour, water resources, industrialisation, agriculture, geography and trade as strategic opportunities. The document is blunt about the required fundamentals: infrastructure, energy, transport, ICT, science, technology, land, urban development, human resources, peace and security.

Uganda’s challenge is conversion. Oil must become industrial capability, not only fiscal revenue. Agriculture must become processing, storage, exports and rural income. A young population must become productivity rather than political pressure. Its location between Kenya, Rwanda, South Sudan, Tanzania and DRC must become logistics income rather than border friction. Uganda’s vision cannot be fully realised inside Uganda alone. Its market is regional, its corridors are regional, and its energy and food-security logic are regional.

Rwanda is the execution state. Vision 2050 is built around economic growth and prosperity, and high quality of life for Rwandans. Its pillars, human development, competitiveness and integration, agriculture for wealth creation, urbanisation and agglomeration, and accountable and capable institutions, reflect a country that treats state capability as an economic asset.

Rwanda’s constraint is size. Its advantage is discipline. It needs regional corridors, regional markets, regional services exports and deeper access to DRC, Tanzania, Uganda, Burundi and Kenya. For Kigali, integration is not ceremonial. It is economic infrastructure. A small, land-linked economy aiming for high-income status has no choice but to make borders less expensive.

Burundi is the equity-and-state-renewal economy. Its revised national plan, aligned with the ambition of becoming emerging by 2040 and developed by 2060, rests on state commitment, economic efficiency, social equity, sustainable ecology and heritage, and fruitful partnerships. Its priorities include structural transformation, basic social services, governance, reconciliation, ecology, international cooperation, import substitution, export promotion and local transformation of raw materials.

That makes Burundi one of the clearest cases where growth and legitimacy must move together. The country needs roads, power, agricultural productivity, processing capacity, investor confidence and a stronger public-delivery system. Its regional opening lies in becoming a compact agro-industrial and services economy plugged into Rwanda, Tanzania and eastern DRC. Its risk is being bypassed by faster-moving corridors unless it improves execution speed.

Somalia is the maritime frontier. Its National Transformation Plan is framed around governance, economic transformation, social and human capital, and climate resilience. That sequence matters. Somalia’s development problem begins with state capability: security, law, institutions, public finance, federal coordination and predictable rules.

Yet Somalia brings assets that change the EAC map: coastline, ports, fisheries, livestock, trade networks, diaspora capital and proximity to the Gulf of Aden and Red Sea routes. Its membership pushes the EAC deeper into the Indian Ocean economy. If stabilised, Somalia can become a ports, fisheries, livestock and trade-services frontier. If integration runs ahead of institutions, however, it risks adding complexity to an already fragile state-building process.

South Sudan is the peace-first resource frontier. Its development agenda is shaped by the reality that peace is the first economic infrastructure. Oil, land, livestock, water and location give the country significant long-term potential. But without security, roads, public financial management, service delivery and institutional continuity, those assets remain stranded.

For the EAC, South Sudan is a frontier with high upside and high implementation risk. A stable South Sudan could become a food, livestock, energy and logistics bridge linking East Africa to Sudan, Ethiopia and the wider Nile Basin. An unstable South Sudan remains a regional cost. Its national vision therefore depends less on another growth slogan and more on whether the state can convert peace into production.

DRC is the continental-scale mineral and market multiplier. Its strategic development priorities, governance, economic diversification, human capital, infrastructure, territorial planning and sustainable provincial growth, speak to a country whose central challenge is not lack of assets but lack of conversion systems.

Congo gives the EAC mineral depth, hydropower potential, forests, agricultural land, industrial-market scale and strategic access into Central Africa. But it also brings the bloc’s biggest coordination burden: insecurity in the east, weak infrastructure, administrative fragmentation and dependence on raw extraction. If the EAC can help stabilise corridors, harmonise customs, support power interconnection and build mineral value chains, DRC becomes the bloc’s biggest multiplier. If not, its scale remains underpriced potential.

The EAC’s own strategy is supposed to bind these national roles into a functioning market. Its integration ladder, customs union, common market, monetary union and eventual political federation is designed to reduce trade friction, deepen mobility and enlarge the economic space. Its regional priorities mirror the national visions: infrastructure, agriculture and food security, industrialisation, tourism, trade, services, human capital, peace and security, digital transformation, natural-resource management and climate resilience.

That overlap is important. East Africa’s national visions are not contradictory. They are incomplete without each other.

Industrialisation and value addition form the second major convergence. The countries no longer want to remain exporters of raw crops, minerals, livestock, oil or unprocessed commodities. Tanzania is looking at industrial scale and transformative sectors. Kenya is pushing manufacturing and services competitiveness. Uganda wants to turn agriculture, oil and minerals into productive capacity. Rwanda is pursuing high-value competitiveness. Burundi is emphasising local transformation of raw materials. DRC’s logic depends on moving from raw extraction to mineral value chains. Somalia and South Sudan need productive sectors that can stabilise livelihoods and public revenues. For the EAC, industrialisation only becomes viable if countries coordinate production rather than duplicate the same industries in small domestic markets.

Tanzania’s logistics ambition needs Ugandan, Rwandan, Burundian and Congolese cargo. Kenya’s financial and services economy needs regional firms to scale. Uganda’s agro-energy transformation needs markets, corridors and industrial demand. Rwanda’s high-income strategy needs regional access. Burundi’s state-renewal strategy needs regional trade and investment. Somalia’s recovery needs institutional integration and maritime commerce. South Sudan’s peace dividend needs markets and infrastructure. DRC’s resource transformation needs security, power, infrastructure and regional value addition.

This is where the EAC must move from treaty language to economic engineering.

Agriculture and food security are common to every vision, even when expressed differently. Rwanda calls it agriculture for wealth creation. Uganda sees agriculture as a major national opportunity. Tanzania, Burundi, South Sudan and DRC have major land and water potential. Kenya has commercial agriculture, finance, logistics and agro-processing capacity. Somalia has livestock and fisheries. This creates a strong regional case for food systems integration: grains, dairy, meat, fisheries, horticulture, coffee, tea, oilseeds and processed foods can become cross-border value chains. The EAC’s food-security agenda should therefore move beyond emergency response and become an industrial policy for rural transformation.

Food is the obvious starting point. A regional food system would reduce imports, stabilise prices, create rural employment and support agro-processing. Instead, too much of the region still treats food security as a national emergency rather than a shared production opportunity.

Energy security and power interconnection are another shared priority. Industrialisation cannot happen without affordable, reliable and increasingly clean energy. Tanzania is placing energy among its strategic drivers. Uganda has hydropower and oil. Kenya has geothermal and renewable capacity. DRC has massive hydropower potential. Rwanda and Burundi need affordable regional power. South Sudan has oil and future generation potential. Somalia needs energy systems that support recovery and production. The regional opportunity is an EAC power market where generation, transmission and demand are planned across borders. Energy should become one of the strongest pillars of regional industrialisation.

Digital transformation and innovation are becoming the new layer of integration. Kenya has the region’s most visible private-sector technology ecosystem. Rwanda has built a strong digital-governance identity. Tanzania identifies digital transformation, science, technology and R&D as development drivers. Uganda includes ICT and science, technology, engineering and innovation among its fundamentals. Burundi is pushing public-service digitalisation. Somalia has strong telecom dynamism. South Sudan and DRC need digital tools for state administration, revenue systems, market formalisation and service delivery. For the EAC, digital integration means interoperable payments, customs systems, digital IDs, trade certificates, business registries, tax systems and data-governance frameworks.

Industrialisation will require discipline. Every country wants factories. Not every country can build the same factories. The EAC will need to organise production around comparative advantage rather than political vanity. Kenya can deepen services, finance, pharmaceuticals, technology and light manufacturing. Tanzania can anchor logistics, agro-processing, fertiliser, mining, energy and heavier industry. Uganda can push agro-industry, oil-linked manufacturing and food systems. Rwanda can specialise in high-value services, light manufacturing, conferences, tourism and digital platforms. Burundi can focus on agro-processing, textiles and compact manufacturing. Somalia can scale livestock, fisheries, ports and trade services. South Sudan can start with food, livestock, energy and basic manufacturing. DRC can anchor green minerals, batteries, hydropower and heavy industrial potential.

Human capital and skills development sit at the centre of the visions. Every country recognises that young populations only become an advantage when they are educated, healthy, skilled and productively employed. Tanzania calls it human capabilities and social development. Rwanda places human development as a pillar. Kenya links quality of life to education, health and productivity. Uganda treats human resources as a fundamental. Burundi focuses on basic social services and social equity. Somalia, South Sudan and DRC need human capital as part of state rebuilding and economic inclusion. The EAC’s role is to harmonise qualifications, support labour mobility, build regional centres of excellence and connect education systems to priority sectors such as logistics, agriculture, energy, manufacturing, digital services and health.

Youth employment and demographic transformation cut across every national plan. East Africa’s population is young and expanding. This can become the region’s greatest asset or its largest source of pressure. The visions all imply the same policy requirement: jobs must grow faster than expectations. Industrialisation, agriculture, services, digital platforms, tourism, construction, logistics and the green economy must absorb millions of young people. The EAC can support this through labour mobility, regional skills recognition, entrepreneurship finance and cross-border business opportunities.

Governance, peace and security are the most decisive convergence areas because all other ambitions depend on them. Tanzania treats peace, security and stability as a foundation. Rwanda emphasises accountable and capable institutions. Kenya’s political pillar focuses on accountable governance. Uganda includes peace, security and defence among its fundamentals. Burundi links transformation to governance, peace and reconciliation. Somalia’s first transformation pillar is governance. South Sudan’s development framework is peace-first. DRC’s development challenge is inseparable from governance and security, especially in the east. The EAC cannot build a common market on insecure corridors, weak institutions or mistrust. Peace and governance are therefore economic infrastructure.

The political economy will be hard. Non-tariff barriers persist. Border delays still drain competitiveness. Domestic politics often rewards protectionism. Security crises spill across borders. Infrastructure projects move at different speeds. Some economies fear domination by larger neighbours. Others fear premature exposure of domestic firms.

But the alternative is weaker. Individually, most East African economies are too small to compete at the scale required by global manufacturing, digital services, food-security markets and energy-transition supply chains. Together, they form one of Africa’s most consequential economic corridors: Indian Ocean ports, Great Lakes markets, Nile Basin routes, Red Sea access, mineral belts, agricultural zones, tourism circuits and one of the world’s youngest populations.

Climate resilience and environmental sustainability now cut across the region’s visions. Tanzania’s Dira 2050 has environmental integrity and climate resilience as a pillar. Rwanda includes climate and sustainability in its long-term planning logic. Burundi places ecology and heritage among its pillars. Somalia’s plan includes environment and climate resilience. DRC’s development priorities include sustainable development and balanced provincial growth. Kenya, Uganda and South Sudan face major climate pressures in agriculture, water, livestock, energy and urbanisation. For the EAC, climate action should be treated as a regional competitiveness issue: climate-smart agriculture, disaster early warning, renewable energy, forest protection, water management, sustainable tourism and blue economy cooperation are no longer optional.

Natural resources, minerals and the green economy are another major point of convergence. DRC brings world-scale minerals and hydropower potential. Tanzania has mining, gas, agriculture, forests, tourism and blue economy assets. Uganda has oil, minerals, water and agriculture. Kenya has geothermal, tourism, agriculture and services. Somalia has fisheries, livestock and maritime assets. South Sudan has oil, water, land and livestock. Burundi and Rwanda have minerals, agriculture and tourism potential. The regional challenge is to stop exporting value too early. Minerals, energy, fisheries, forests, wildlife and agricultural land should be linked to processing, conservation, green finance and industrial value chains.

Trade integration and market access are where the national visions meet the EAC most directly. Every country needs larger markets to justify industrial investment. Rwanda and Burundi need access because of small domestic markets. Uganda needs regional buyers for food, energy-linked industry and manufactured goods. Tanzania and Kenya need cargo, consumers and regional production links. Somalia needs trade normalisation. South Sudan needs markets for a future peace dividend. DRC needs regional connectivity to unlock its scale. The EAC Customs Union and Common Market are therefore not abstract treaties; they are the commercial machinery that can make national visions investable.

The real measure of success will not be whether each country publishes another vision document. It will be whether goods can move from Dar es Salaam to Bujumbura without crippling delays; whether Kenyan capital can finance Tanzanian, Somali or South Sudanese infrastructure; whether Ugandan food can reach eastern Congo efficiently; whether Rwandan services can scale across borders; whether Congolese minerals can be processed inside the region; whether Somali ports can complement Mombasa and Dar es Salaam; and whether young East Africans can study, work, trade and build companies beyond their national borders.

Private-sector development and investment mobilisation appear across the visions as countries try to move beyond state-led planning into productive capital formation. Kenya’s model is strongly market-facing. Tanzania wants a robust private sector and an improved investment climate. Uganda’s opportunities require private investment in oil, agriculture, industry, tourism and infrastructure. Rwanda’s high-income ambition depends on productivity, firm growth and investment discipline. Burundi and Somalia need partnerships and investor confidence. South Sudan and DRC need capital that can operate despite higher perceived risk. The EAC can strengthen this by harmonising investment rules, reducing non-tariff barriers, deepening capital markets and supporting bankable regional projects.

Urbanisation and productive cities are an emerging convergence. Rwanda explicitly treats urbanisation and agglomeration as a pillar. Kenya’s development model depends heavily on Nairobi, Mombasa and secondary cities. Tanzania’s growth will be shaped by Dar es Salaam, Dodoma, Arusha, Mwanza, Mbeya, Tanga and Zanzibar. Uganda’s Kampala metropolitan pressures are central to productivity. DRC, Somalia, Burundi and South Sudan all face fast-growing urban systems that need planning, services, housing and jobs. The EAC should treat cities as economic infrastructure. Productive cities reduce logistics costs, concentrate skills, support manufacturing and create service sector scale.

Regional financing and implementation discipline are the final convergence areas. The visions are capital-intensive. Infrastructure, power, industrial parks, climate resilience, education, health systems and digital platforms require financing at a scale many national budgets cannot meet alone. The EAC’s opportunity is to help structure regional projects that can attract development finance, pension funds, sovereign funds, commercial banks and private investors. But money alone will not be enough. The region also needs disciplined implementation, measurable targets, stronger institutions and fewer policy reversals.

East Africa’s national visions are ambitious because the region has no low-risk alternative. Its population is growing, cities are expanding, climate shocks are intensifying and global competition is becoming more unforgiving. The old model, export raw commodities, import finished goods, negotiate donor support and manage fragmented national markets, cannot deliver the incomes now promised in official plans.

The next model has to be regional, industrial, digital, green and institutionally credible.

That is the quiet message inside the region’s blueprints. Tanzania’s Dira 2050, Kenya’s Vision 2030, Uganda Vision 2040, Rwanda Vision 2050, Burundi’s 2040/2060 ambition, Somalia’s transformation plan, South Sudan’s peace-and-development framework and DRC’s strategic plan are not separate stories. They are chapters in the same economic negotiation.

The market is larger than any one country. The infrastructure is too expensive to duplicate. The resources are too strategic to export raw. The labour force is too young to underuse. The climate risks are too severe to manage alone. The security challenges are too interconnected to contain within borders.

For the EAC, the task is no longer to sell the idea of integration. It is to make integration function like infrastructure: quietly, predictably and every day.

Uchumi360

Business Intelligence

Uchumi360

Business Intelligence

Uchumi360 covers business, investment, and economic policy across East, Central, and Southern Africa.

For the serious reader

You read to the end. That places you in a small group.

Uchumi360 is built for readers who demand precision over speed, structure over sentiment, and analysis that holds uncomfortable conclusions rather than softening them. If this work sharpens how you think about Africa's economy, help us keep building the infrastructure behind it.

Institutional Partners

Commission intelligence. Shape the conversation.

Uchumi360 works with development finance institutions, investment firms, sovereign bodies, and strategic organisations across the coverage region. Institutional partnership unlocks:

- Commissioned sector and country intelligence reports

- Branded research series under your institution's authority

- Exclusive data briefings for internal strategy teams

- Speaking and editorial presence at Uchumi360 events

- Co-published investment outlooks for your markets

Support Our Work

Independent analysis has a cost. Help us bear it.

Uchumi360 does not carry advertising. It does not take editorial direction from sponsors. Every article is produced without commercial compromise. Your contribution funds the reporting, research, and editorial infrastructure that keeps this analysis free from influence.

Secure checkout: One-time and monthly support are processed securely. Add payment credentials to enable checkout here.

Stay Connected

Keep up with every new insight.

Follow our latest analysis, policy coverage, and market intelligence as soon as it is published. If you need something specific, reach out directly and we will point you to the right research.